Stocks Slide After Jobs Report Sends Mixed Messages About U.S. Economy

Stocks on Wall Street slid on Friday after a report on the state of the labor market sent mixed signals about the economic recovery and as market turbulence triggered by the Omicron variant continued.

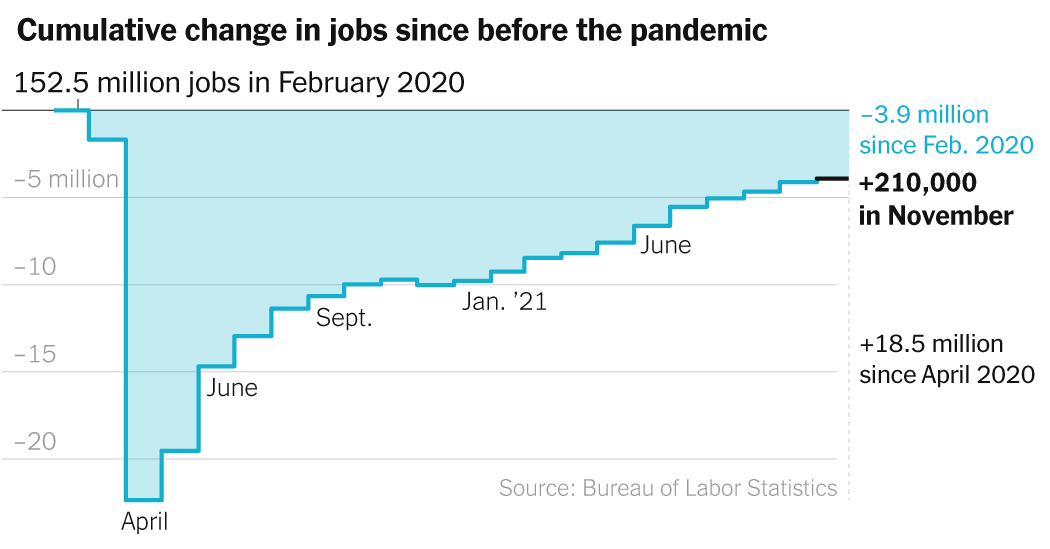

U.S. employers added 210,000 jobs in November, the Labor Department said on Friday, far below expectations for a 550,000 gain and a sharp slowdown from October. But the report also showed that the unemployment rate had dropped, and the overall participation rate, which measures the proportion of Americans who either have jobs or are looking for one, rose to its healthiest level since the start of the pandemic.

Trading was volatile, as it has been all week. The S&P 500 closed about 1 percent lower after starting the day with a small gain. In the bond market, the yield on the 10-year U.S. Treasury dropped nine basis points, or 0.09 percentage points, to 1.35 percent, a sign that investors were moving money to the relative safety of government bonds.

The muddled jobs report added to economic uncertainty brought on by the Omicron variant of the coronavirus, which has led to renewed pandemic restrictions.

Adding to the recent turbulence are shifting expectations for how quickly the Federal Reserve will wind down a bond-buying program put in place early in the pandemic — a move that is a precursor to interest rate increases, which are expected to begin next year. Friday’s jobs report wasn’t weak enough to change the market’s view that the Fed could push up the timing of rate increases as it looks to tamp down inflation.

“Beyond the disappointing headline number, which could be owing to seasonality quirks, the rest of the report is actually pretty strong and is unlikely to deter the Fed from its hawkish turn earlier in the week,” Fiona Cincotta, senior financial markets analyst at Forex.com, said in a note to clients.

Technology stocks were particularly hard-hit on Friday, and the tech-heavy Nasdaq composite dropped 1.9 percent. Apple, Alphabet, Facebook, Microsoft and Amazon were all lower. Together, those five companies account for more than 20 percent of the market value of the S&P 500, with movements from these stocks having a large impact on the direction of the stock market.

Investors had been pulling back on tech stocks all past week, with the Nasdaq outpacing the S&P 500’s declines.

“The market might have been a little too optimistic on the outlook for tech,” said Edward Moya, a senior market analyst at Oanda, a foreign currency exchange and brokerage firm. “Now they’re taking that risk off the table.”

Also weighing on the S&P 500 on Friday was Tesla. Shares of the electric vehicle-maker, which climbed above a market valuation of $1 trillion in October, fell more than 6 percent. The drop on Friday came a day after the company’s founder, Elon Musk, disclosed that he had sold another $1 billion in Tesla stock. Mr. Musk, who has been selling shares in part to cover tax obligations related to the exercise of stock options, has sold nearly $11 billion worth of the shares in recent weeks. But because he’s also gaining new shares thanks to those stock options, Mr. Musk’s stake in Tesla actually stands slightly higher.

Friday capped a tumultuous week for stock investors, which began after evidence of a new coronavirus variant was first reported by South Africa, prompting travel restrictions in several countries. Wall Street ended the day higher on Monday before dropping again on Tuesday after the Fed’s announcement that it would withdraw financial support from the economy quicker.

The first case of the Omicron variant in the U.S. was detected on Wednesday, driving shares lower. The S&P 500 is down nearly 4 percent since Omicron first began to make headlines.

Travel and leisure stocks continued to fall on Friday. Norwegian Cruise Line and Carnival were both down about 4 percent. Airline stocks were also lower.

Oil prices, which have been particularly unsteady in recent days, were slightly lower, with West Texas Intermediate, the U.S. crude benchmark, down 0.4 percent $66.26 a barrel after earlier having climbed above $69 a barrel.

On Thursday, officials from OPEC, Russia and other oil-producing countries said they would continue with a previously agreed-to program of gradually adding oil to the market.

Shares of the Chinese ride-hailing company Didi Chuxing plunged more than 22 percent after the company announced Friday that it would delist its shares from the New York Stock Exchange in favor of a listing in Hong Kong. Other Chinese companies listed in New York also fell, including the e-commerce giant Alibaba, which fell about 8 percent, and JD.com, which slid about 7.7 percent.

Image

April

June

Sept.

Jan. ’21

April

–3.9 million jobs since Feb. 2020

+18.5 million since April 2020

+210,000

in November

152.5 million jobs in February 2020

American employers reported weaker-than-expected hiring last month. But a survey of American workers showed a surge in the number taking jobs.

Those conflicting pictures emerged from a single government report on Friday, further clouding the economic outlook as a new phase of the coronavirus pandemic unfolds.

The ambiguous Labor Department data muddles the calculations of Federal Reserve policymakers weighing whether to shift their focus from creating jobs to reining in prices. It is a complication for a White House trying to show the success of its economic course. And it offers little guidance to businesses about what to expect in the months ahead.

To be sure, recent economic readings were already a muddle. Consumer confidence readings have been at a low ebb, even as Americans continue on a spending spree. Inflation has hit levels unseen in decades, but investors seem unperturbed.

Part of the puzzle on Friday arose because the Labor Department report is based on two surveys, one polling households and the other recording hiring among employers.

The survey of employers showed the addition of just 210,000 jobs in November on a seasonally adjusted basis, the year’s weakest showing. Economists had forecast a second straight gain of more than 500,000.

But good news abounded in the household survey, which showed that the total number employed, seasonally adjusted, jumped by more than 1.1 million. The unemployment rate fell to 4.2 percent from 4.6 percent.

“I don’t know that I’ve ever seen such an extraordinary gap between the two surveys,” said Diane Swonk, chief economist for the accounting firm of Grant Thornton in Chicago.

The overall participation rate, which measures the proportion of Americans who either have jobs or are looking for one, rose by 0.2 percentage point to 61.8 percent, its healthiest level since the pandemic hit. The rate for prime-age workers, 25 to 54 years old, also edged up.

74

76

78

80

82

84%

Jan. ’19

Jan. ’20

Jan. ’21

There was a big increase in participation last month among Hispanic men and women, who were among the hardest hit by the pandemic.

Still, the lackluster hiring number was a reminder of the on-again, off-again pattern in the labor market since the pandemic began nearly two years ago. This month, job gains in businesses where face-to-face contact is required — like stores, restaurants, bars and hotels — were especially soft.

Retail employment dropped by 20,000 last month on a seasonally adjusted basis, while hiring in leisure and hospitality industries rose by 23,000, compared to a gain of 170,000 in October. The white-collar sector, which has largely shrugged off the worst effects of the pandemic, remained a source of strength, with a 90,000 jump in employment in professional and business services.

Hiring at factories jumped by 31,000, while transportation and warehousing gained nearly 50,000 workers, an indication of how online commerce is picking up speed ahead of the holidays.

Leisure and hospitality

+23,000

in November

16.9 million jobs in Feb. 2020

Business and professional services

State and local government

Despite a fairly tight labor market, the economy is still roughly four million jobs short of prepandemic levels. About one-third of those positions are in the leisure and hospitality sector, which is vulnerable if the Omicron variant — which came to public attention after the November job surveys were conducted — turns out to be as much of a threat as the Delta strain.

“That’s the risk but it probably won’t show up before Christmas,” said Scott Anderson, chief economist at Bank of the West in San Francisco. “It could be an issue in the new year. We’re still dealing with the Covid pandemic and the risks are there for the economy and hiring.”

Many labor market analysts argue that there’s much room from employment growth because so many people have yet to return to the labor force, and because businesses overall are in a sturdy financial position with the capacity to expand both supply and their payrolls.

“To me, the most important question in the economy going forward is: Will companies improve jobs enough to entice people back into employment, and to face those higher risks?” said Aaron Sojourner, a professor at the University of Minnesota and a former economist at the Council of Economic Advisers for the previous two administrations. “The big wild card is the virus and our public health efforts, and second is the Fed and how they adjust.”

Throughout the fall, the economy’s path has been characterized by clashing signals.

The “quits rate” — a measurement of workers leaving jobs as a share of overall employment — has been at or near record highs, which suggests that workers are confident they can navigate the labor market to find something better. But the University of Michigan’s survey of consumer sentiment dropped to levels not seen since the sluggish recovery from the recession of 2007-9.

The report noted “the growing belief among consumers that no effective policies have yet been developed to reduce the damage from surging inflation.” Shoppers are facing the steepest inflation in 31 years. In October, prices increased 6.2 percent from a year earlier.

Nonetheless, markets remain relatively calm. The major stock indexes are up by impressive levels this year. And bond yields, which tend to move higher in inflationary environments, remain near record lows, indicating that investors don’t see inflation as a longer-term threat to the economy or financial stability.

In recent days, the chair of the Federal Reserve, Jerome H. Powell, has faced pressure from different political camps to focus more tightly on price increases.

Critics of the Fed say the central bank’s “accommodative” bond-buying policies — which have kept borrowing costs low and led to a large and continued increase in the money supply — went on too long and were irresponsible in light of an already aggressive emergency response from Congress.

Fed officials, including Mr. Powell, still maintain that the price increases mainly reflect pandemic aberrations that will dissipate. But in congressional testimony on Tuesday, Mr. Powell signaled a pivot from revitalizing the economy to keeping a lid on prices.

“The economy is very strong, and inflationary pressures are high,” he said. “It is therefore appropriate in my view to consider wrapping up the taper of our asset purchases.”

Economists are divided over the potential impact of a winter coronavirus surge. Some say it could cool off the economy, easing inflation, because it could inhibit in-person activities. Others say a new wave could raise prices further by complicating the logistics of supply chains.

John C. Williams, president of the Federal Reserve Bank of New York, told The New York Times on Wednesday that the new variant could “mean a somewhat slower rebound overall” yet “increase those inflationary pressures, in those areas that are in high demand.”

For consumers, one potentially positive effect of renewed virus fears is the recent pullback in energy prices, which have risen substantially this year. The spikes have been particularly intense for fuel oil — which is used for industrial and domestic heating — and for crude oil, which directly translates to gasoline prices at the pump.

One cure for increasing prices is for consumers’ take-home pay to keep up with them. And with many businesses eager to attract workers, wages for nonsupervisory workers continued their upward climb. Average hourly earnings were up 8 cents in November, to $31.03, and are 4.8 percent higher than a year ago — though that rate is exceeded by the most recent inflation readings.

Ben Casselman contributed reporting.

Maybe the labor shortage isn’t quite as bad as it looked.

One of the great mysteries of the U.S. economy in recent months has been the glacially slow return of workers. From August 2020 through October 2021, the share of adults who were working or actively looking for work barely budged — even as employers posted a record number of job openings, and raised wages to try to fill them.

In November, however, the labor force grew by nearly 600,000 people — the biggest gain in more than a year — and the number of Americans reporting that they were working rose by more than 1.1 million, according to a Labor Department report released Friday.

Those big gains might be confusing given that the same report showed that employers added just 210,000 jobs in November, less than half as many as in October and far below forecasters’ expectations. The seeming paradox can be explained by the fact that the two sets of numbers come from separate surveys: one of employers and one of households.

Over time, the two data sources usually tell relatively consistent stories about the job market. But they sometimes diverge over shorter periods, because of differences in what they measure and errors inherent in any survey.

For about the past half year, the survey of households had been showing significantly weaker job growth than its sister survey — until last month, when it was much stronger. Economists generally put more trust in the employer survey, which has a much larger sample size. So the recent pattern suggests that the household survey had been undercounting employment and, in effect, caught up in November.

If that interpretation is correct, it means the household survey data released Friday overstates the one-month jump in the labor force. But it also implies that the labor force wasn’t as stagnant in recent months as previous monthly jobs reports implied. (The household survey data doesn’t get revised, unlike the employer survey, which has been repeatedly revised upward in recent months.)

Stronger labor force growth would be welcome news for policymakers at the Federal Reserve, who have been worried that the slow return of workers could contribute to inflation. Still, the data released Friday doesn’t indicate that the shortage has been fully resolved. Wages rose significantly in November, suggesting employers are still struggling to hire, and there are still 2.4 million fewer people in the labor force than before the pandemic began.

Image

President Biden on Friday cheered what he called the “extraordinary strides” the U.S. economy has made since he took office, claiming credit for the fastest calendar-year drop in the unemployment rate in American history.

His remarks came after the Labor Department reported that the jobless rate fell to 4.2 percent in November, from 4.6 percent in October and 6.7 percent in November 2020.

The optimistic spin was an example of Mr. Biden’s growing challenge in talking about the economy. He and his aides see the accelerating recovery from pandemic recession since winter as a validation of his policies — including the $1.9 trillion package he signed in March, the American Rescue Plan — and a marked improvement on the pace of the rebound from the 2008 financial crisis.

But he has been forced to acknowledge that many Americans do not feel that improvement, and instead have grown more pessimistic about the economy and his handling of it as the country experiences high gasoline prices and its fastest overall inflation in several decades.

All presidents accentuate the positives from monthly jobs reports, and Mr. Biden’s Friday remarks were no different. In addition to falling unemployment, he stressed wage gains and the creation of more than 6 million jobs since he entered the White House in late January, and he played down the news that the economy created 210,000 jobs for the month, less than half of what most economists had expected.

“Every year, December brings the joys of a holiday season and gives us an opportunity to reflect on the year gone by and look ahead and begin to imagine the new year to come,” he said. “This year, we can reflect on an extraordinary bit of progress. Our economy is markedly stronger than it was a year ago.”

“Thanks to the American Rescue Plans, we’re cutting child poverty in America by more than 40 percent,” Mr. Biden said a moment later, “and millions of children who spent last Christmas in poverty will not bear that burden this holiday season.”

But as he has done repeatedly in recent weeks, Mr. Biden proceeded to acknowledge the economic pain and frustration that many Americans are feeling, particularly from rising prices but also from the continued spread of the pandemic, which is killing around 1,000 Americans each day.

He also made clear that he sees the new strategy that he laid out this week to combat Covid over the winter as the most important policy tool at his disposal to further help the economy — and persuade voters that the recovery is benefiting them.

“Despite this progress, families are anxious,” he said. “Anxious about Covid. They’re anxious about the cost of living, the economy more broadly. They’re still uncertain. I want you to know I hear you. It’s not enough to know that we’re making progress. You need to see it and feel it your own lives around the kitchen table and your checkbooks.”

Republicans hammered Mr. Biden for the disappointing job gains without acknowledging the big drop in the unemployment rate. The Republican National Committee called it “the worst jobs report of the year.” Representative Kevin Brady of Texas, the top Republican on the Ways and Means Committee, was even more dour. “This is a miserable jobs report,” he said, “there’s no spinning it any other way.”

Twitter’s new chief executive, Parag Agrawal, said on Friday that he would reorganize top leadership at the company and that two key executives would depart.

The shake-up was the first sign of change under Mr. Agrawal, who took the reins of the social media company on Monday after its co-founder and chief executive, Jack Dorsey, announced his resignation.

Twitter has been under pressure from investors to introduce new products more quickly and add to its revenue, and Mr. Agrawal said in an email to Twitter employees that the leadership changes were designed to accelerate Twitter’s pace.

Twitter’s head of engineering, Michael Montano, and its head of design and research, Dantley Davis, will leave by the end of the year. Mr. Davis had championed a culture change at Twitter that pushed staff for higher performance and that some employees criticized as bullying.

Twitter confirmed the executive departures in a regulatory filing on Friday.

Mr. Davis played a key role in a behind-the-scenes effort over the past two years to remake Twitter’s culture. But he repeatedly clashed with employees because of his blunt style. His treatment of workers was also the subject of several investigations by Twitter’s employee relations department and of complaints to Mr. Dorsey that too many people were leaving.

Mr. Davis and Mr. Montano will remain advisers to Twitter during the first quarter of 2022, according to the regulatory filing.

Mr. Dorsey, Mr. Davis and Mr. Montano are not the only executives who have recently announced plans to leave Twitter. The company’s head of people, Jennifer Christie, also announced that she would leave by the end of the year, according to two people familiar with the announcement who were not authorized to speak publicly.

The product and engineering teams within Twitter will be consolidated under three executives, a Twitter spokeswoman said.

Kayvon Beykpour will manage all consumer products, including design and research for those products. Revenue products, including designers and researchers, will be overseen by Bruce Falck. And Nick Caldwell will manage the technical infrastructure on which Twitter runs, overseeing data science and back-end engineering.

Twitter announced in February that it aimed to double revenue and add 123 million more active users by 2023, and the company hopes that consolidating Twitter’s teams under a handful of leaders will help it execute on its plans more quickly, a spokeswoman said.

The United States faces a default sometime between Dec. 21 and Jan. 28 of next year if Congress does not act to raise or suspend the debt ceiling, the Bipartisan Policy Center warned on Friday.

The projection was a more narrow window than the nonpartisan think tank previously provided last month and the group suggested that the actual deadline, or X-date, could be in the earlier end of that range.

Democrats and Republicans appear to have tempered their tone around the latest debt limit standoff this time around, yet there is no current plan for lifting the borrowing cap. Republicans continue to insist that Democrats must act alone to address the issue, while Democrats have countered that raising the borrowing cap is a shared responsibility given that both political parties have incurred big debts over the last several years.

“Those who believe the debt limit can safely be pushed to the back of the December legislative pileup are misinformed,” said Shai Akabas, BPC’s director of economic policy. “Congress would be flirting with financial disaster if it leaves for the holiday recess without addressing the debt limit.”

Treasury Secretary Janet L. Yellen warned lawmakers in November that the United States could be unable to pay its bills soon after Dec. 15.

During testimony before the Senate Banking Committee this week, she underscored the urgency of the matter.

“I cannot overstate how critical it is that Congress address this issue,” Ms. Yellen said. “America must pay its bills on time and in full. If we do not, we will eviscerate our current recovery.”

After approaching the first default in American history, Congress in October raised the statutory debt limit by $480 billion, an amount the Treasury Department estimated would allow the government to continue borrowing through early December.

The Bipartisan Policy Center said that there is additional uncertainty surrounding the debt limit this year because of the pandemic and the various economic relief programs that are still ongoing.

Dec. 15 is particularly important because the Treasury Department is required to make a $118 billion payment to the Highway Trust Fund. If corporate tax receipts that are due that day come in weak, Treasury could face a cash crunch and the United States would be unable to fully meet all of its obligations like paying out Social Security and funding military paychecks.

The Congressional Budget Office said earlier this week that it expected that Treasury might run out of cash by the end of December if Congress fails to act. The C.B.O. suggested, however, that Treasury might be able to defer some Highway Trust Fund payments, which were mandated in the recently passed infrastructure law, potentially staving off a default until sometime in January.

The Treasury Department said on Friday that it would not label any country a currency manipulator but that it was keeping Taiwan, Vietnam and Switzerland on notice over their currency practices.

In its biannual foreign exchange report, the department also criticized China’s lack of transparency in its currency practices and said it had significant concerns about the impact of China’s actions on American companies and workers.

“Treasury is working relentlessly to promote a stronger and more balanced global recovery that benefits American workers, including through close engagement with major economies on currency-related issues,” Treasury Secretary Janet L. Yellen said in a statement.

The report continued the more conciliatory tone that the Biden administration has shown in international economic diplomacy compared with the Trump administration, which used the currency manipulation label to punish China for its trade practices. Under the Trump administration, Vietnam and Switzerland were also labeled manipulators.

Being labeled a currency manipulator requires a trading partner to enter into negotiations with the United States and the International Monetary Fund to address the situation. The blemish is somewhat symbolic but can lead to tariffs or other retaliation if talks collapse.

In April, the Biden administration said that Taiwan, Vietnam and Switzerland met the criteria to be considered currency manipulators but that it was not going to formally apply the label, noting extraordinary economic conditions brought on by the pandemic. The United States reached an agreement with Vietnam in July to address currency concerns, and the Treasury Department said on Friday that it was continuing to manage its progress and to negotiate with Taiwan and Switzerland.

The Treasury Department said that it would closely monitor the foreign exchange activities of China’s state-owned banks. A Treasury official said that the United States has raised concerns with Chinese officials about how these institutions intervene in currency markets.

“China’s lack of transparency and use of a wide array of tools complicate Treasury’s ability to assess the degree to which official actions are designed to impact the exchange rate,” the report said.

The United States placed China, Japan, South Korea, Germany, Ireland, Italy, India, Malaysia, Singapore, Thailand, Mexico and Switzerland on its “monitoring list” of trading partners whose currency practices warrant close attention.

BuzzFeed is off to a rocky start on the road to becoming a public company. Shareholders on Thursday voted on its deal with a special purpose acquisition company, or SPAC, as BuzzFeed News union employees staged a daylong strike over contract negotiations. The merger was approved, but the company said it had raised only $16 million from the deal, far less than the over $250 million it had hoped for.

Because investors do not know what company a SPAC plans to acquire, they have the opportunity to redeem their shares at the I.P.O. price before a merger is official. When a SPAC’s shares trade below this price, as has been the case with BuzzFeed’s merger partner, these redemptions can be significant, leaving a company with less money than expected when it agreed to a deal. This highlights a major challenge for companies engaging in SPAC deals, the DealBook newsletter reports, making this popular route to market less attractive.

SPAC redemption rates have been around 50 percent this year, up from 20 percent last year, according to Dealogic. Companies that relied on this cash have responded to redemptions by adding debt financing to deals (BuzzFeed has a $150 million convertible note to fall back on) and by rewriting the terms of mergers.

But the biggest SPAC deal of all bucked the trend. Grab, the Singapore-based “super app,” began trading on Nasdaq on Thursday after closing its roughly $40 billion SPAC merger with almost no redemptions. Shares of Altimeter, the SPAC buying Grab, have been trading above their I.P.O. price for months, and investors may also be heartened by a $4 billion private investment that accompanied the deal. Grab is also more established than many other companies that have recently gone public via a SPAC.

Investors are “really starting to understand the benefits of a super-app business model that’s very distinct from what you see in the U.S.,” Grab’s president, Ming Maa, told DealBook.

Low redemptions, though, don’t guarantee a smooth first day of trading. Grab’s stock closed Thursday down 21 percent, which may be partly because Grab structured its deal to allow most employees, aside from senior executives, to sell their shares. (Altimeter’s chief executive, Brad Gerstner, has called employee share lockups “one of the most insidious things” about the traditional I.P.O. process.) There was also heavy interest from short-sellers in the stock.

The proliferation of SPACs, alongside a hot market for traditional initial public offerings, has made 2021 the first year since 1997 that the number of public companies has increased, according to Bank of America. This follows years of worries that regulation made it too onerous to become a public company, leading start-ups to stay private for longer and depriving retail investors of the chance to buy into promising firms. SPACs have made it easier and faster for companies to go public, but recent trends might lead some to question whether it was worth it.

Image

Royal Dutch Shell said Thursday that it had decided not to invest in a British oil development off the coast of Scotland that has become a test of the government’s environmental credentials.

The field, known as Cambo, is in deep water northwest of the Shetland Islands. It is seen as a bellwether for the future of Britain’s declining but still large North Sea oil industry.

The British government is considering whether to approve the project, which environmental groups and some politicians have said should be rejected because it would produce carbon dioxide emissions responsible for climate change.

Shell, which owns 30 percent of Cambo, said it had “concluded the economic case for investment in this project is not strong enough at this time.”

The company also said there was “potential for delays,” apparently referring to the possibility that the drilling would draw protests from environmental groups and possibly legal actions trying to stop it. Shell said recently that it planned to move its headquarters from the Netherlands to Britain.

Shell’s decision to decline to invest in developing Cambo is a serious blow to the project. Siccar Point Energy, a private equity-backed firm that is Cambo’s main owner and developer, said that while “disappointed” by Shell’s decision, it remained “confident about the qualities” of the project, saying it would create 1,000 jobs.

Siccar Point has said that it plans to invest $2.6 billion in Cambo and that it has already spent $190 million in the four years since it acquired the rights to the field, which was discovered in 2002.

The oil industry argues that as long as Britain consumes more oil and natural gas than it produces, it is preferable for those fuels to come from the North Sea, where emissions regulations can be set, instead of from places with potentially fewer controls.

The environmental group Greenpeace UK said letting Cambo go ahead “would be a disaster for our climate and would leave the U.K. consumer vulnerable to volatile fossil fuel markets.”

-

Didi Chuxing, the Chinese Uber-like ride-hailing champion and once considered the world’s most successful start-up, said Friday that it would begin delisting its New York-traded shares and prepare for a public offering in Hong Kong.

The move is sure to reverberate outside China, particularly in Washington and on Wall Street. Just in June, Didi sold shares to global investors in an initial public offering in New York that valued the company at $69 billion. The abrupt turn after just six months is likely to anger investors, who bid up the price of the company this summer when it listed. READ MORE →

-

Google will no longer require employees to start returning to the office on Jan. 10 because of “continued uncertainty,” the company said Thursday. Google had targeted early January as the soonest that it would demand employees to come to the office a few times per week as part of its hybrid work schedule. In an email on Thursday, Google did not set a new mandatory return to the office date, saying different regions will assess conditions next year.

Source: https://www.nytimes.com/live/2021/12/03/business/jobs-report-stock-market

{kind=link}