Will Experian Boost help your credit score? Here’s what to know

CNN —

CNN Underscored reviews financial products such as credit cards and bank accounts based on their overall value. We may receive a commission from Experian if you sign up for Experian Boost via the links on this page, but our reporting is always independent and objective.

Having a good credit score is important, since a strong score can give you access to the very best loans, mortgages and credit cards. But what if your credit score isn’t very good? Or you have a limited history with credit? Lenders can be reluctant to approve people with poor credit scores for new credit cards or loans, which makes it even harder to build — or rebuild — your credit history.

While there are a lot of “credit repair” companies that claim to fix your credit, they can be expensive, and it’s not always clear which ones have a less than stellar track record. However, there’s a relatively new way to potentially increase your credit scores in just a few minutes — and it’s free.

The feature is called Experian Boost™*, and it’s definitely legit. In fact, Experian® is one of the three main credit reporting agencies in the United States and has been in business for over 20 years, so it has a lot of experience with credit scores. But does Experian Boost actually improve your FICO® Score**, which is utilized by 90% of top lenders? Let’s take a look.

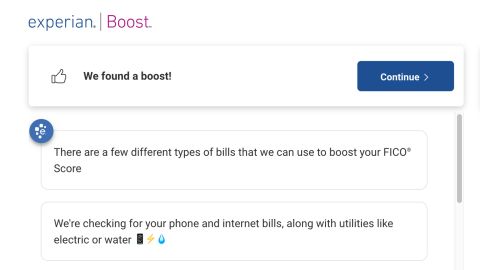

Experian Boost is designed to help give people credit where credit is due. By providing your information to Experian, you can get credit for on-time payments that aren’t normally part of your credit history, such as utility, telecom, cable and some streaming service payments.

On-time payments account for 35% of your FICO® Score, so if you’ve been on the ball in paying your utility bills, phone bills and even your Netflix® streaming service payments each month, you can add them to your credit report and potentially boost your FICO Score***.

Related: What’s a good credit score?

When you access Experian Boost, it allows you to connect your checking, savings and other bank or credit card accounts that you use to pay your monthly bills so that your payment history can be added to your Experian credit file.

As long as you have at least three consecutive months of payments within the last six months from the same account, Experian Boost will pick up positive payment activity and add it to your Experian credit file. Best of all, it won’t report negative payments — only those that were paid on time.

Click here to increase your credit scores for free with Experian Boost.

The Boost process is quite easy and takes just a few minutes. After creating an Experian account, you then link your financial institutions where you maintain your checking, savings or other bank or credit card accounts that you use to pay your bills, and enter your login credentials to seamlessly link them.

If you have multiple accounts at the same financial institution, Experian allows you to select which accounts you want included so you can just add the accounts you use to pay your bills.

Once you’ve linked your accounts, Experian will automatically go through all your recent transactions and identify payments that qualify to be added to your Experian credit file, such as utility bills. It then shows you a list of eligible bills and allows you to select which ones you want to add to your report.

Experian Boost keeps you informed as it searches for potential payments that can improve your credit scores.

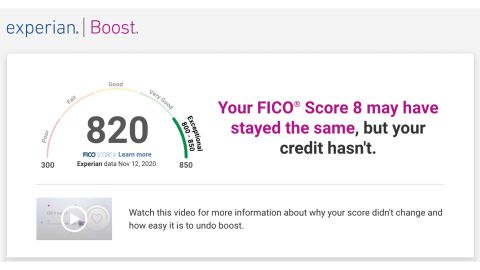

Make your selections and within moments, Experian Boost factors in the new information and shows you your new (hopefully improved) FICO® Score. Since Experian Boost doesn’t include missed payments, your FICO Score won’t go down, but it might not change if there either isn’t enough information from the added accounts or your FICO Score is already relatively high.

Even if it doesn’t make a difference to your FICO® Score, the process is as easy as it sounds and literally costs nothing. And once you have it all set up, Experian Boost will continue to monitor your payments, and may increase your credit scores if future payments make a difference.

Use your on-time payments to improve your credit scores with Experian Boost.

It depends. According to Experian, US users have boosted their FICO® Scores by close to 45 million points, and the average FICO Score has increased 12 points when using Experian Boost. Those with little to no credit history and those with very poor to fair credit generally see the biggest FICO Score increases.

We tried Experian Boost ourselves and found the process to be very straightforward, but we didn’t see any increase in our credit scores. That’s likely because the CNN Underscored reviewers who tried it already pay their bills on time and have high credit scores to begin with.

Our reviewers didn’t see any change to our FICO® Score with Experian Boost, but people with little to no credit history and those with very poor to fair credit generally see the biggest increases.

But people who pay their bills through their bank account and don’t have a longstanding credit card or loan history may see a bigger impact. That’s because you’ll start to fill in your “payment history” component of your FICO® Score, which is one of the most important factors in a credit score.

There aren’t really any true disadvantages of Experian Boost — the worst that can happen is it doesn’t change your FICO® Score. It doesn’t cost anything, and it won’t hurt your credit, so the only thing you might lose is a few minutes of your time to set it up. The Experian membership also provides your FICO Score for free on an ongoing basis, which is useful to have as you work to improve your credit rating.

However, there are a few caveats to keep in mind. First, Experian Boost only adds these positive payments to your Experian Credit Report — it can’t add any information to reports from other credit agencies, such as Equifax or TransUnion. So if you apply for a credit card and the lender pulls your credit report from another bureau, the lender won’t see boosted credit scores.

Related: Does opening a new credit card hurt your credit score?

You’ll also find that the tool doesn’t work for bills that aren’t in your name, even if you contribute to them. For example, if you live with roommates and send your portion of the gas bill to your roommate via Venmo or PayPal, or give them a check or cash, Experian Boost won’t pick up those payments.

Finally, some people aren’t comfortable providing their bank login to a third party. According to Experian, when you use Experian Boost, Experian only uses your bank credentials to capture your ongoing positive payments and identify any potential new boosts.

For additional protection, Experian also makes sure the name and address on your bank account matches what’s on your Experian membership profile. Still, if you’re concerned about privacy, you might decide that the upside of Experian Boost isn’t worth handing over your personal information.

If your FICO® Score could use some help, there’s essentially no downside to trying Experian Boost.

Frankly, yes, especially if your credit scores could use some help. Not everyone’s FICO® Score will increase with Experian Boost, but the service is free, and it only takes a few minutes to enter your information and connect your accounts. There’s very little downside to using the feature, and you can always remove the added payment history from your Experian credit file down the line if you want.

The best way to permanently improve your credit scores is to methodically whittle down your debt by paying your loans, mortgages and credit card bills on time every month. But that process can take time, so in the interim, try potentially giving your credit scores a little boost for free with Experian Boost.

Learn more about improving your credit scores with Experian Boost.

*Results may vary. Some may not see improved scores or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost.

**Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO Score than FICO Score 8, or another type of credit score altogether. Learn more.

***Experian and the Experian trademarks used herein are trademarks or registered trademarks of Experian and its affiliates. The use of any other trade name, copyright or trademark is for identification and reference purposes only and does not imply any association with the copyright or trademark holder of their product or brand. Other product and company names mentioned herein are the property of their respective owners.

Source: http://rss.cnn.com/~r/rss/cnn_topstories/~3/-I11TxbI1iM/index.html

{kind=link}